Focus on Real Output per Hour Worked

This assignment provides instructions on building the graph below and includes writing prompts for out-of-class assignments.

Using GeoFRED® to Compare Labor Productivity Growth Across States

This assignment provides instructions on creating the map below and suggests prompts for in-class discussion. See how you do on our sample discussion question below.

Click on the map above to view an interactive version.

Question: Name the state with the highest labor productivity growth during 2020. Don’t overlook Hawaii and Alaska!

Storytelling with Data and FRED Interactive Modules

Index Numbers: Learn how to use several FRED® features to use index numbers to measure growth in prices: changing the data units and applying a formula to the data. The FRED Interactive modules can be embedded in your learning management system.

Quiz Yourself on Productivity

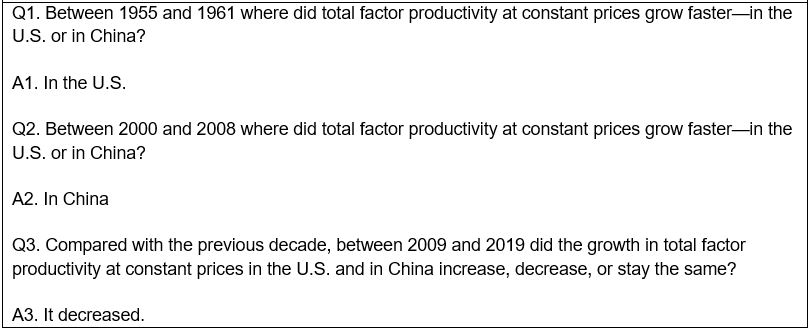

Q1. Between 1955 and 1961 where did total factor productivity at constant prices grow faster—in the U.S. or in China?

Q2. Between 2000 and 2008 where did total factor productivity at constant prices grow faster—in the U.S. or in China?

Q3. Compared with the previous decade, between 2009 and 2019 did the growth in total factor productivity at constant prices in the U.S. and in China increase, decrease, or stay the same?

Q1. Between 1988 and 2008 where did labor productivity grow faster—in the durable or in the non-durable manufacturing sector?

Q2. Compared with the years between 1988 and 2008, between 2009 and 2019 did labor productivity in both durable and non-durable manufacturing increase, decrease, or stay the same?

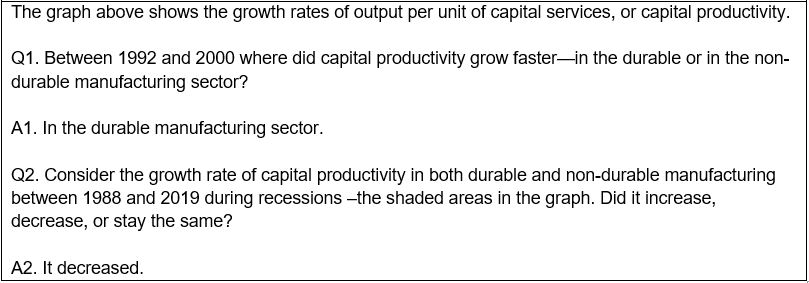

The graph above shows the growth rates of output per unit of capital services, or capital productivity.

Q1. Between 1992 and 2000 where did capital productivity grow faster—in the durable or in the non-durable manufacturing sector?

Q2. Consider the growth rate of capital productivity in both durable and non-durable manufacturing between 1988 and 2019 during recessions –the shaded areas in the graph. Did it increase, decrease, or stay the same?

Now that you’ve aced this quiz, give it to your students using this dashboard. To customize this dashboard, just click the “Save to My Account” button at the top of the dashboard.