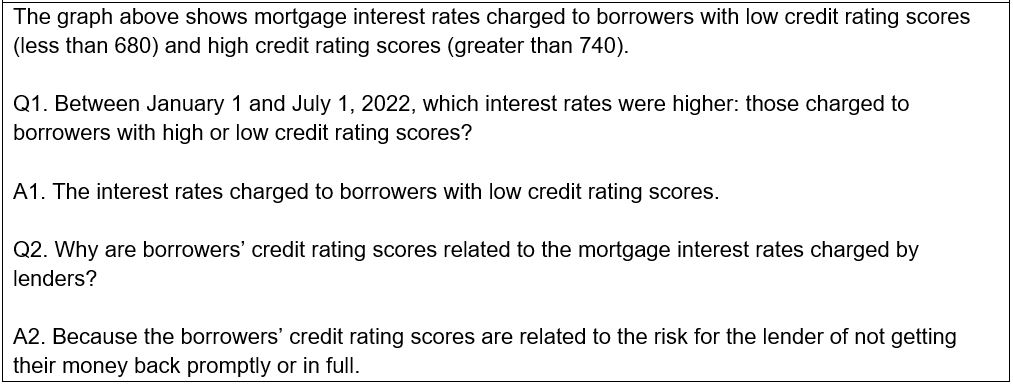

On November 17, Freddie Mac made a number of enhancements to the Primary Mortgage Market Survey® to improve the collection, quality, and diversity of the data. Instead of surveying lenders, the weekly results are now based on thousands of applications received from lenders across the country that are submitted to Freddie Mac when a borrower applies for a mortgage. Additionally, the PMMS® will no longer publish fees/points or adjustable rates. More information can be found here.

With these changes, FRED has discontinued five series, as follows:

- Margin for 5/1-Year Adjustable Rate Mortgage in the United States (DISCONTINUED)

- Origination Fees and Discount Points for 5/1-Year Adjustable Rate Mortgage in the United States (DISCONTINUED)

- Origination Fees and Discount Points for 15-Year Fixed Rate Mortgage in the United States (DISCONTINUED)

- Origination Fees and Discount Points for 30-Year Fixed Rate Mortgage in the United States (DISCONTINUED)

- 5/1-Year Adjustable Rate Mortgage Average in the United States (DISCONTINUED)

Freddie Mac will continue to update these two series, which will remain in FRED: